![Heaader1SourceAccount[3148]](https://sourceaccounting.ca/wp-content/uploads/2021/11/Heaader1SourceAccount3148-2048x289.png)

In this final part of our series, we focus on income splitting with children—a strategy significantly limited by Canada’s attribution rules. These rules are designed to prevent parents from transferring income to minor children to reduce the family’s overall tax burden.

If you haven’t read Part 1 (understanding attribution rules and how they work) and Part 2 (strategies for splitting income with a spouse), we strongly recommend reviewing those first to get the full context and build a clear understanding of the framework we’re working within.

Part 1 – Understanding the Basics of Attribution Rules

Part 2 – Strategies for Income Splitting with a Spouse Within Attribution Limits

Now, let’s explore how attribution rules apply when income or assets are transferred to children and what planning opportunities, if any, still exist.

1) Gift to adult child – When you gift an asset to an adult child (age 18 or older), no attribution rules apply—all future income (investment, capital gains, or business income) is taxed in the child’s hands, not yours. For attribution rules, a child is considered an adult if they are 18 or older by December 31 of the tax year. Attribution generally applies only to minor children, not to adult children or other adult family members. However, the gift triggers a deemed disposition at fair market value, and you must report any capital gain or loss on your tax return. Once the asset is in the child’s name, they may invest or use the funds as they wish. If they choose to contribute to their own TFSA or RRSP or use the funds toward a principal residence, these can be excellent long-term income-splitting and tax-planning strategies. While you can’t contribute directly to your child’s TFSA/RRSP, you can gift cash, and they can contribute themselves.

2) Use of a family trust–Instead of transferring assets directly to your child, you can set up a family trust and transfer assets to it. This approach is often used when there are valid reasons not to give assets outright—for example, the child is a minor, has limited financial experience, is facing potential marital or legal issues, has medical or cognitive limitations, or you wish to maintain control over when and how the funds are used. A trustee (you or someone you appoint) manages the trust assets and controls income distributions to the beneficiaries (e.g., your children). This allows for income splitting while preserving oversight and protection. Here are the key things to remember.

- If the beneficiary is a minor child, attribution rules apply to certain types of income—such as dividends, interest, and rental income—and that income will be taxed in your hands. However, capital gains are not subject to attribution, and when distributed by the trust, they will be taxed in the beneficiary’s hands. As such, it may be more tax-efficient for minor children to invest in growth-oriented assets over income-producing ones.

- One way to avoid attribution is to loan funds to the trust at the CRA’s prescribed interest rate. If the trust pays the interest due by January 30 of the following year, attribution rules will not apply. In this case, income earned inside the trust can be distributed and taxed at the child’s (often lower) marginal rate.

- If the beneficiaries are adult children, attribution rules generally do not apply. You may gift the funds outright or use the prescribed rate loan strategy. In both cases, any income or gains distributed to the adult child will be taxed in their hands.

3) Use of a discretionary family trust. Where the beneficiaries include a mix of minor and adult children, the use of a discretionary family trust is often recommended. A discretionary trust gives the trustee the authority to decide how and when to allocate income or capital among the beneficiaries based on their judgment and within the guidelines and objectives set out by the trust deed (typically drafted at the direction of the settlor—you).

This structure allows for flexible, year-by-year income allocation, enabling the family to adapt distributions based on each beneficiary’s tax position, personal needs, or financial circumstances. It’s beneficial when you want to preserve control over timing, manage exposure to attribution rules for minors, or protect family assets from risks such as divorce, creditor claims, or lack of financial maturity.

4) Use of Lifetime Capital Gains Exemption (LCGE). Suppose your child is a shareholder in a Qualified Small Business Corporation (QSBC). In that case, they may be eligible to claim the Lifetime Capital Gains Exemption (LCGE)—which can shelter up to $1,016,836 (2024 limit, indexed) in capital gains from tax when the shares are sold. This strategy is often used in estate freezes or succession planning, where parents freeze the value of their shares and allow future growth to accrue to children or a family trust for their benefit. Proper structuring and meeting QSBC conditions are critical to avoid CRA challenges.

5) Registered Education Savings Plan(RESP). An RESP is a popular and effective tool to help fund your child’s post-secondary education. Income earned inside the plan, such as interest, dividends, and capital gains, is tax-deferred while it remains in the account. Additionally, the federal government contributes through programs like the Canada Education Savings Grant (CESG) and, for lower-income families, the Canada Learning Bond (CLB).

The original contributions are not taxed when the funds are eventually withdrawn to pay for education. In contrast, the accumulated income and government grants are taxed in the student’s hands, who often pay little or no tax due to being in a low-income bracket. You can contribute up to $50,000 per beneficiary over the lifetime of the plan.

6) Registered Disability Savings Plan (RDSP). An RDSP is a long-term savings plan designed to provide future financial support for an individual with a disability. The beneficiary must be approved for the Disability Tax Credit (DTC). In many cases, the beneficiary can be the plan holder and contributor if they are legally capable. However, a parent or guardian can also open and manage the plan on their behalf.

You can contribute up to $200,000 per beneficiary over their lifetime, with no annual contribution limit, as long as the contributions stay within the lifetime maximum and are made before the end of the year when the beneficiary turns 59. The federal government also contributes through the Canada Disability Savings Grant (CDSG) and Bond (CDSB).

All earnings and government contributions grow tax-deferred, and withdrawals are taxed in the hands of the beneficiary, who often has little or no other income. This structure helps ensure long-term care and support and can be part of broader income-splitting and estate-planning strategies

7) Income splitting for business owners. If you own a business, one common income-splitting strategy is to employ family members in legitimate roles within your business. This allows you to shift income to a family member in a lower tax bracket. However, any salary or wages paid must be reasonable, market-based, and supported by documentation (e.g., job descriptions and payroll records) in case of a CRA review.

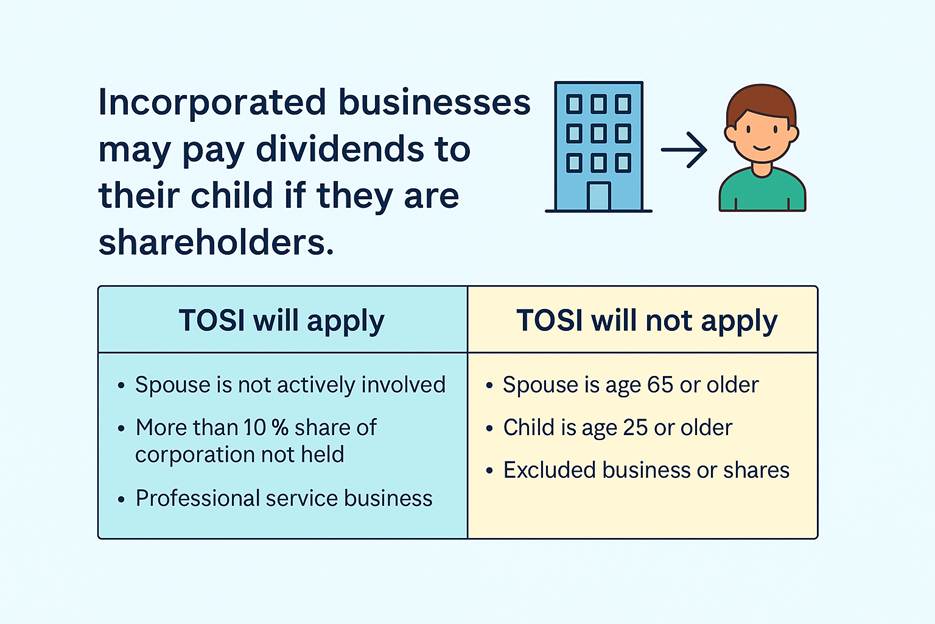

8) Dividends to Children from an Incorporated Business. If your business is incorporated, you may also pay dividends to your children if they are shareholders. However, you must be mindful of the Tax on Split Income (TOSI) rules, which can significantly limit the tax benefits of this strategy. TOSI generally applies when income is split with a family member who does not make a meaningful contribution to the business—such as by working in the business on a regular basis, owning at least 10% of the shares (by votes and value), or having made a capital investment.

If these conditions are not met, dividends may be taxed at the highest marginal rate, eliminating the advantage of income splitting. For this reason, TOSI-compliant structuring is essential when planning dividend strategies involving family members.

9) Support a Child-Owned Business. If your adult child starts their own business, it can be a practical and fully compliant way to achieve income splitting within the family. When your child operates their own active business, any income they earn from it will be taxed in their own hands, not yours—even if you help finance the business through a gift, loan, or investment. This strategy avoids attribution rules, provided the child genuinely operates the business and is not merely a vehicle to redirect your income. In more advanced structures, you may consider incorporating the child’s business and supporting it through a loan or minority investment while allowing your child to retain control. As long as the business income flows to your child and they are actively involved, this is a clean and effective method of shifting income away from your higher tax bracket.

Other family members. While many of the strategies discussed here focus on children, most can also be applied to other adult family members, such as siblings, parents, or nieces and nephews, because the attribution rules generally do not apply to non-dependent adults. However, care must be taken where TOSI rules apply, especially when splitting dividend income or investment income with related individuals who are not actively involved in the business.

Throughout this 3-part blog series, we’ve covered the key aspects of attribution rules and income-splitting strategies for Canadian families:

- In Part 1, we explained attribution rules, who they apply to (spouses, minor children), and how they differ from the Tax on Split Income (TOSI).

- In Part 2, we explored several income-splitting strategies with a spouse, such as gifting, prescribed rate loans, salaries, and dividends — all while staying within the CRA’s compliance framework.

- Part 3 (this blog) focused on strategies involving children and other family members, including trusts, RESPs, RDSPs, hiring family, and planning around the Lifetime Capital Gains Exemption.

These tools can create meaningful tax savings, help build intergenerational wealth, and reduce your family tax burden.

While these strategies can be powerful, they are complex. If not implemented correctly, they can lead to unexpected tax consequences or missed opportunities. It’s essential to approach income splitting with care and proper planning.

Whether you’re a physician in GTA, a medical professional or other professional in Mississauga or Brampton, or running a family business in Toronto, if you’re considering any tax planning strategies, getting professional advice tailored to your family’s situation is highly recommended. Book a call by calling at 647-930-8130

Additional Sources: CRA Websites:

- Frequently asked questions – Income sprinkling

- Guidance on the application of the split income rules for adults

Tax Planning for High-Net-Worth Families & Medical Professionals in Mississauga & Toronto. Source Accounting Professional Corporation is a trusted CPA firm serving professionals and business owners across the GTA, including Toronto, Brampton, Oakville, Milton, and Etobicoke. We specialize in customized tax strategies for doctors, dentists, pharmacists, nurses, consultants, and realtors—helping you reduce taxes through income splitting, estate planning, and wealth transfer strategies. 📞 Call 647-930-8130 to book a consultation with an experienced tax advisor.

Disclaimer: The above contents are provided for general guidance only, based on information believed to be accurate and complete, but we cannot guarantee its accuracy or completeness. It does not provide legal advice, nor can it or should it be relied upon. Please contact/consult a qualified tax professional specific to your case.