![Heaader1SourceAccount[3148]](https://sourceaccounting.ca/wp-content/uploads/2021/11/Heaader1SourceAccount3148-2048x289.png)

This article delves into several common questions business owners often have about HST/GST in Canada. It aims to dispel misconceptions even experienced business owners may hold, which can be costly when the CRA reviews their files. HST/GST is a complex topic, and it is highly advisable to have a correct understanding from the outset and seek professional advice when needed.

Are all provinces on the HST system?

Traditionally, the federal government and provinces had their own sales tax regime called General Sales Tax (GST) and Provincial Sales Tax (PST), respectively. Businesses were required to register with the Canada Revenue Agency (CRA) for GST and provincial tax departments for PST and file returns separately for each.

To simplify and streamline the process, the federal government and some provinces implemented a Harmonized Sales Tax (HST) system. As of now, five provinces in Canada have adopted the HST system, and they are referred to as “participating provinces.” In other provinces, businesses must charge GST for the CRA and PST for their respective provinces. Consequently, HST and GST are used interchangeably in this article. Nevertheless, it’s important to note that PST rules vary for each province.

The current HST rates in these provinces are as follows:

HST participating provinces and rates.

- Ontario 13%

- New Brunswick, Newfoundland and Labrador, Nova Scotia, and Prince Edward Island 15%

Other (non-participating) provinces

- Alberta— Only 5% GST Alberta is the only province with no PST.

- British Columbia 5% GST + 7% PST

- Manitoba 5% GST + 7% PST

- Northwest Territories 5% GST + 5% PST

- Saskatchewan 5% GST + 6% PST

- Quebec 5% GST + 9.975% PST

- Nunavut 5% GST + 5% PST

- Yukon 5% (GST) + 5% PST

I am a new business; do I need to register for HST?

Every business making taxable supplies (products or services) in Canada must register for HST/GST, except for ‘small suppliers’. Businesses that make only exempt supplies are not required to register. For some businesses like taxi services, you must register even as a “small supplier.”

Who is a small supplier?

You are a small supplier if your (and associated group’s) worldwide sales are less than $30,000, including zero-rate sales in the last four consecutive quarters.

My sale is less than $30,000 in one year. Do I need to register?

Many businesses are caught in this trap. They mistakenly believe they are exempt from HST/GST registration because their sales are under $30,000 in one year. However, it’s crucial to recognize that to qualify as a small supplier, sales must remain under $30,000 in the last four consecutive quarters. These quarters may spread across different years. They become aware of the issue when the CRA conducts an audit after a span of 3 to 4 years, issuing a notice of re-assessment with hefty payment due for uncollected HST, along with accrued interest and penalties.

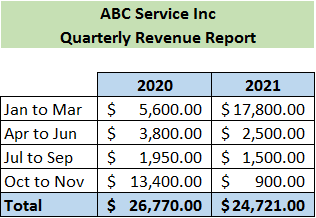

The below example of ABC Service Inc. will explain it.

How most business owners would think:

As can be seen from the table below, neither in 2020 nor in 2021 ABC Service Inc. crossed the threshold of $30,000 in sales. Accordingly, most business owners will think that ABC Services Inc. does not have an obligation to register for HST.

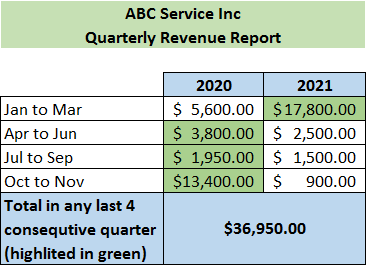

How the CRA would consider the information

However, the CRA does not look at sales for the year. It considers the last four quarters, which may not be in the same year. Now, in the table below for ABC Service Inc., CRA will consider four consecutive quarters starting from Apr 2020 to Mar 2021 that have total sales of $36,950. Accordingly, the company is no longer a small supplier and must register for HST.

As a new business, I am already registered for HST. When should I start charging HST? Should I wait to reach the $30,000 sales threshold?

Once you register for HST, you must charge HST in each invoice regardless of your sales volume. Otherwise, your business will be responsible for reimbursing the CRA for any HST not collected, from your pocket.

What do I do with the HST collected? Do I include it in my income?

HST collected is not considered income; instead, it represents your liability to the government/CRA. HST/GST is a tax that you collect as an agent of the government from the buyer. You collect this money, keep track of it, and remit it to the CRA.

Is the HST paid on business purchases considered an expense?

No, it is not. One of the advantages of HST registration is that when you purchase supplies for business use (for resale or use in business consumption), you can claim a refund of the HST paid, which is known as an Input Tax Credit (ITC). Therefore, any HST paid by a business is not considered an expense.

Since I am a small supplier, can I or should I register for HST?

As mentioned earlier, all businesses must register for HST if they sell taxable supplies, with the only exception being small suppliers. However, there is no restriction on the registration of small suppliers. In fact, most businesses choose to register for HST from day one, which is recommended in most cases. The reason is straightforward. Once you register for HST, you can claim refunds for the HST/GST you pay on your purchases.

Besides the financial perspective, it’s important not to present yourself as a ‘small supplier’ to your buyers. In many cases, other businesses may feel uncomfortable doing business with you if you don’t have an HST/GST number. So, it’s wise to register for HST to appear professional and establish trust with your business partners.

What are zero-rated supplies?

Zero-rate supplies, as the name suggests, are those on which you charge HST at a rate of 0%. Common examples of zero-rate supplies include basic groceries, prescription drugs, and export supplies, which otherwise would not be zero-rated when sold within Canada.

The advantage of designating a supply as zero-rated is that these businesses can register for HST. This means that even though these businesses will not charge HST (or charge at the rate of 0%), they can still claim a refund of HST paid by them, called Input Tax Credit (ITC).

What are exempt supplies? Is exempt supply the same as a zero-rated supply?

Exempt supplies are different from zero-rated supplies.

Exempt supplies are the ones that are exempt from HST application. The most common examples of exempt supplies are the sale of a used house, music lesson, insurance, financial products, and most medical services performed by licensed physicians or dentists.

From the customer’s perspective, zero-rate and exempt suppliers are the same, as they don’t pay any HST on their purchases. Both make a product or service less expensive for the end user. However, there is a massive difference from the business perspective. Generally, exempt supply is not good news for a business making exempt supplies since it can not register for HST and cannot get a refund of HST paid.

I have other businesses that are registered for the HST. I am starting a new business and should I register this for HST only when I reach the threshold of $30,000?

This is another myth or misconception about the HST/GST registration requirements. For the purposes of HST registration requirements, you and the companies under your control are considered as a group. Therefore, if you have other businesses with taxable supplies of $30,000 or more, you must register the new business for HST/GST from day one because, as a group, you are already over the $30,000 limit.

Frequently, we encounter business owners who receive substantial bills from the CRA for HST/GST not collected, plus interest and penalties, a couple of years after starting a new business. This occurs because they were unaware of the requirement to register for HST and collect it right from the beginning.

I registered a business for HST, but the business didn’t get going; do I need to file an HST return?

This is another common area of confusion for business owners who think they only need to file an HST/GST return if they are running a successful business. Regardless of your business performance, you must file HST/GST at the given frequency.

I have stopped the business; I am no longer operating it; do I still need to file an HST return?

Incorrect; you must still file HST returns until your HST account is officially closed. To close your HST account, you need to request it from the CRA. Even after asking for the closure, you must file HST/GST returns till the date the HST account is closed and remit any HST collected before the closure.

I did not claim some ITC in the return. Can I still claim it?

It’s worth noting that ITCs don’t have to be claimed in the same period. If you forgot to claim ITCs in the current period, don’t worry; you have a four-year time limit to claim them. This four-year limit applies to businesses with sales under $6 million, with some exceptions. Businesses with higher sales may have a shorter time limit for claiming ITCs.

My corporation has two business lines. One makes taxable supplies, and the other makes exempt supplies. Can I claim ITC on all the purchases I made for both businesses since I am HST registered?

You can claim ITC only for purchases made for taxable supplies. If you only sell exempt supplies, the CRA will not register you for HST/GST. However, if your corporation sells exempt and taxable supplies, your corporation can register for the HST/GST. However, you can claim an ITC refund only for supplies made for producing taxable supplies. If a supply is used by both products (taxable and exempt), then you need to devise a reasonable formula to allocate HST/GST to each supply.

I am a business in Ontario; will I charge 13% HST on all my supplies?

You charge HST/GST based on the location of your customer or where services or products are delivered, not your location. These rules are called the place of supplies rule, and sometimes, these rules can become very complicated. However, the examples below help us understand the basic concept and work for most cases.

For example, IT consultants providing services to another company in Ontario will charge 13% HST, which is the rate in Ontario. But if you do the same service for a client in Alberta, you will charge 5% because the GST rate for Alberta is 5%. Similarly, if you provide the same service to a client in the USA or any other country, you will charge HST/GST at 0% (it will be treated as a zero-rated supply).

I am a corporation’s director; if the corporation does not pay HST, will CRA only pursue the corporation or am I personally liable?

This is yet another misconception about the corporation and the responsibility of directors. As a general rule, you, as a director, are personally responsible for ensuring that the corporation files and pays taxes to the CRA. Remember, the CRA has extensive power under the regulations and can use it to make your life difficult. So, make sure if you are listed as the director of a corporation, you have a good handle on what is happening with the corporation and that the corporation is up to date with tax obligations.

If you leave the corporation, ensure you properly resign, which is recorded in the corporation’s records. In some cases, individuals have assumed that they are no longer related to the corporation, and the CRA has come knocking on the door after years, making the director personally liable for the corporation’s HST dues.

Can I charge HST for the purchases made before registering for HST?

A corporation or any HST registrant can only claim ITC for a period after the registration. Any HST paid on expenses before registration is not refundable. The only exceptions are inventory on hand, capital assets based on the tax cost of the assets, and prepaid expenses related to a period after registration.

Conclusion:

HST/GST is a highly complex subject. In this article, we have only scratched the surface of it. It is essential to fully understand the HST/GST rules as they apply to you, which can be daunting for any business owner. It is highly critical that you obtain professional advice from a CPA to navigate this process and obtain the guidance that a business needs from time to time.

In our next article, we have also discussed how to avoid CRA audits. CRA audits are stressful and challenging to navigate, consuming a significant amount of a business’s time and energy. The good news is that by following some good practices, you can reduce the chances of being audited.

If you require assistance with HST/GST registration, bookkeeping, or tax filing, the Source Accounting Team is well-equipped to assist you. Schedule a consultation call by dialing 647-930-8130.

Source Accounting Professional Corporation (CPA) is a full-service accounting firm in Mississauga, dedicated to individuals, small and medium-sized businesses, providing tax preparation, corporate tax filing, accounting, bookkeeping services, payroll solutions, etc. If you are looking for an accountant Mississauga (Brampton, Toronto, GTA) or an accountancy firm Brampton, you are in the right place.

Disclaimer: The above contents are provided for general guidance only, based on information believed to be accurate and complete, but we cannot guarantee its accuracy or completeness. It does not provide legal advice, nor can it or should it be relied upon. Please contact/consult a qualified tax professional specific to your case.