![Heaader1SourceAccount[3148]](https://sourceaccounting.ca/wp-content/uploads/2021/11/Heaader1SourceAccount3148-2048x289.png)

A family trust is a powerful tool for tax and estate planning. By setting up a trust, you can reduce taxes, protect your assets, and smoothly transfer them to the next generation. The importance of a family trust is particularly pronounced for business owners. In this article, we provide an overview of the family trust, including how it is set up, its legal status, and the benefits and limitations of the trust.

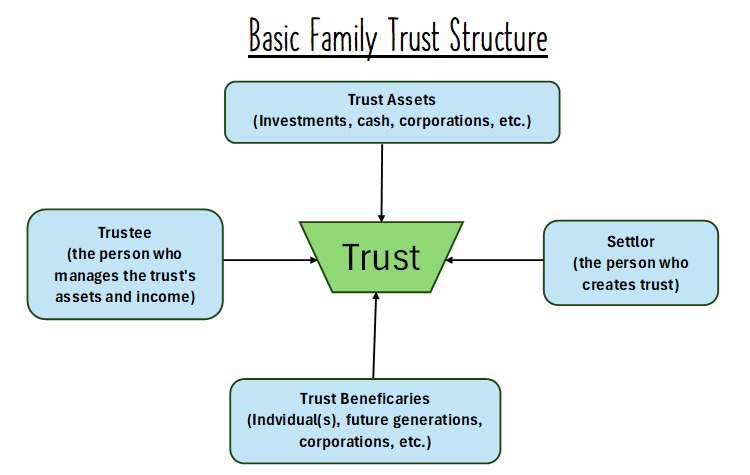

The trust is established when a person (the Settlor) transfers assets or property to the trust for the benefit of the beneficiaries. A trustee is made responsible for the custodianship or administration of the trust and assets for the benefit of the beneficiaries.

Basic Trust Structure:

The Settlor: The Settlor would settle the trust by gifting a value, say a $100 bill. After settlement, the Settlor no longer has a role in the trust. Anyone can be a settlor other than a beneficiary. Once assets are transferred to the trust, they become property of the trust.

The Trustee: A trustee or a group of Trustees would act to control the trust and its assets. Usually, decisions are made by the majority of the votes. In a family trust, trustees are generally the family members (moms and dads) familiar with the family affairs and engaged with the business. However, trustees’ roles are also assigned to external professionals.

A trustee’s role is critical in managing and administrating a family trust. Trustees manage and invest trust assets, make decisions, and distribute assets per the trust’s terms and beneficiaries’ best interests. Trustees must act with integrity and in good faith and always put the best interests of the beneficiaries first.

The Beneficiary: A person or a group of persons (or entity) for the benefit of whom the trust is set up. The Trust deed must specify the list of beneficiaries of the assets under the management of the trust and may include future generations and children. Generally speaking, is it advisable to include more beneficiaries as the trustee can exclude a beneficiary in the future.

Register the Trust: In some situations, trust must be registered. Obtaining professional advice is crucial when establishing a family trust to prevent potential mistakes and ensure proper setup and administration.

Types of Trusts in Canada:

There are two main types of trusts in Canada:

- Testamentary Trust.

This trust is created upon the death of a person by a will or by a court order to support a surviving spouse or family member who has a physical or mental disability.

- Inter Vivos Trust (also referred to as “living trust”).

These trusts are created during a person’s lifetime for various benefits, which we will discuss shortly. There are multiple categories of trust within this group. One important sub-type is a discretionary trust. In a discretionary trust, the Settlor assigns the discretionary power to the trustee to allocate benefits to the beneficiaries at their discretion rather than allocating specific benefits to the beneficiaries with a predetermined formula.

In a family trust situation, trustees (mostly family members) can allocate income to a family member (a beneficiary) in the lowest tax bracket for the year.

A Corporation as a Beneficiary of the Trust:

A corporation can also be a beneficiary of the trust, which offers various benefits, including the following.

- It eliminates excess cash from the operating company to make it qualify for a lifetime capital gain exemption limit.

- The dividend can be distributed to the family trust, and then the trustee (of a discretionary trust) can determine which of the beneficiaries should receive this dividend. In cases where individual beneficiaries do not require the dividend, it may be allocated to the beneficiary corporation. The receiving corporations can receive dividends tax-free.

- Additional credit proofing by removing assets and excess cash from the operating company, which is exposed to creditors or litigation owning to its operational activities.

Benefits of Trust:

Protecting Assets for Beneficiaries (and also FROM beneficiaries):

For various reasons, for example, young age and physical or mental health, you may find it appropriate not to transfer assets directly to the children for the time being. In such situations, you place assets in the trust so that the assets/business remain under the trustee’s supervision while children receive the income from those assets/businesses. After attaining a certain age or completing their education, the assets/business are transferred to the beneficiary.

Other than age or physical limitations, in some circumstances, you might not be comfortable giving assets directly to your children because you are concerned about their lack of financial discipline, and you make sure that assets are protected for them and future generations. A family trust is the solution here.

Control Without Direct Ownership Corporation or The Estate Freeze Strategy:

In a typical business situation where an incorporated business is growing successfully, parents want to maintain control of the company but want the future growth to go directly to their kids; using a family is an option.

The trust ensures that the tax liability at their death is frozen based on the current value of the corporation. An estate freeze is done by parents exchanging their existing common shares with preferred shares locked down at the company’s current market value, and trust subscribed to the new common shares at a nominal value, say $100. Now, any increase in the company’s value belongs to the new shares owned by the trust. According to trust, it will not pay any tax on this growth at the death of the business owners.

For details on how an estate freeze works, read our article here.

Protection From the Creditors:

The family trust protects assets from creditors. Trust assets are held on behalf of its beneficiaries, shielding them from claims of the creditors they have against individual beneficiaries. A discretionary trust protects its beneficiaries. For the purpose of the discretionary trust, the beneficiary is assumed to have no direct ownership of the trust assets. Therefore, a discretionary trust provides no value to the creditors. However, it is pertinent to mention that trust must be created when things are going “well.” If the problem is already brewing, the courts may disallow the protection offered by the creation of trust.

Reduced Income Taxes:

Another benefit of the family trust stems from the fact that it receives income from the assets under control and then passes the income over to beneficiaries (family members) with a lower marginal tax rate. However, with the introduction of the Tax on Split Income (“TOSI”) in 2018, the income splitting benefit has been largely eliminated.

Avoiding Tax on Death:

When a person dies, it is deemed that the deceased has disposed of the property or assets at the fair market value. In most cases, there is a capital gain in the estate return, which needs to be paid before the assets are transferred to beneficiaries. These assets may be transferred to a surviving spouse (“automatic rollover” as per tax law). In that case, tax is deferred until the death of the spouse, or the assets are disposed of by the spouse. However, when a family trust owns the assets (say shares of a corporation), the individual’s death has no tax implication as the assets are owned by the trust, not by the individual.

Avoidance of Probate Fee:

In most provinces of Canada, estates are required to pay probate fee (administration fee) before assets are transferred to the legal heirs. This can be a substantial amount, depending on the value of assets. Again, when a family trust owns the assets, it is not subject to probate because the deceased does not hold the assets.

Multiplying the Lifetime Capital Gain Exemption:

If one individual owns a corporation and later sells its shares, the seller can claim a lifetime capital gain exemption of up to $1,016,836 (the limit for 2024), on which they don’t pay tax. This offers substantial tax savings when you are selling a successful business.

Another major advantage of a family trust is that all beneficiaries can claim a lifetime capital gain exemption limit. When a trust owns a corporation and sells a profitable business, the trust can allocate the capital gain to multiple beneficiaries. In turn, each beneficiary can claim their own LCGE, offering significant benefits.”

How Tax Works With Family Trusts:

- Tax rates for trust income:

Income in inter vivos (“living trust”) is taxed at the top personal tax. Typically, any income the trust receives is allocated to or paid out to the beneficiary, leaving no income for the trust. The income paid or payable (vested) to beneficiaries is deductible for the trust. In turn, beneficiaries report income received from the trust in their personal return and pay tax at their respective marginal tax rate.

The CRA interprets the words “to vest” as giving an immediate, fixed right of present and future possession as distinguished from a contingent right.

- Twenty-one (21) Year Disposition Rules:

In most cases, the trust is deemed to have disposed of all its assets. Accordingly, while the trust lasts long, it can’t last forever. This rule may result in possible capital gains within the trust. This can be avoided by distributing the assets to the beneficiary before the deemed disposition in 21 years.

- Tax Filing Requirements:

A family trust must have a December 31 year-end. A trust must file a Trust Income Tax and Information return (T3) within 90 days after the year-end, which would be March 31 or 30 in a leap year.

- Penalties For Non-compliance:

Failure to file the T3, including new schedules, will be subject to a penalty of $25 per day, with a minimum of $100 and a maximum of $2,500. Gross negligence penalties could also apply, and the penalties will be greater of $2,500 or 5% of the maximum FMV of the property held in the trust in the year. Penalties could also be imposed against the trustees in their personal capacities.

Disadvantages of Family Trusts:

While the family trust offers various advantages, it comes with some disadvantages also, some of which are discussed below:

- The family trust has a limited ability to split income after TOSI rules. Before that, it was easy and common for a corporation owned by a trust to receive income and allocate it to adult family members with a lower marginal tax rate. However, as discussed above, a family trust still offers various tax and retirement planning opportunities.

- Creating Associated Companies: Where a discretionary trust owns a corporation, each beneficiary is considered to have a 100% share of the trust. Where the beneficiary also owns their corporation, both companies will be deemed associated for the purpose of small business deduction, which can reduce the ability of the different families to claim small business limits separately.

Another deeming rule treats parents as owning all shares held by a minor child to determine association and small business deduction limits. While it’s typically recommended to keep the beneficiary list open and broad, in such situations, it is crucial to narrow down the list of beneficiaries to minimize the risk of association.

- Loss of Ownership of Assets: Once you transfer an asset to the trust, it becomes an asset of the trust. You can still maintain (indirect) control over the asset by nominating yourself as the trustee or keeping the power to appoint the trustee. In the case of a business corporation, you can maintain control by having fixed-value voting shares, while the trust holds the non-voting share of the corporation. However, controlling assets and owning are two different things.

- Administrative Burden: Establishing the trust comes with various responsibilities, including accounting, administrative, and reporting requirements. Allow yourself the time to handle these things. If you are someone who is not comfortable with these requirements, please think again before establishing the trust.

- Cost of establishing and maintaining trust: One must consider the Cost of establishing and maintaining a trust. There are costs associated with establishing a trust, transferring the assets, and ongoing costs concerning maintaining compliance and reporting requirements.

- Future Changes in The Law: Potential changes in the law may make some of the trust’s objectives unattainable. Similarly, family and financial circumstances and goals may change over time. Any of this might make a family trust unsuitable for family objectives. It is essential to periodically review all these factors and make adjustments to ensure your goals and trust are aligned with the evolving.

Record-keeping requirements for the family trust:

The trustee is vital for managing a trust, handling tasks like maintaining accurate records, filing annual tax returns, ensuring legal compliance, and regularly updating beneficiaries on the trust’s assets and financial status. Choosing a reliable and experienced trustee is crucial for the trust’s long-term management.

Maintaining accurate records for a family trust is crucial, including

- Retaining bank statements and returned cheques.

- Proper resolutions documenting trust decisions should be prepared and stored, and

- An electronic accounting file should be maintained to facilitate any potential CRA audit of the trust.

Conclusion:

As one can observe, a family trust provides a range of benefits, including asset protection, tax planning, and facilitating the transfer of estates. Despite its apparent simplicity, navigating the nuances, techniques, and compliance requirements can be intricate. Therefore, it is highly advisable to seek the guidance of a professional tax practitioner or tax lawyer.

By its nature, tax planning is an ongoing process, making it imperative to continually explore and consider all possible opportunities, whether they pertain to the present or future. The Source Accounting team in Canada specializes in income tax planning and income splitting, expertly minimizing your exposure to Canadian taxes.

Source Accounting Professional Corporation (CPA) is a full-service accounting firm in Mississauga, dedicated to individuals, small and medium-sized businesses, providing tax preparation, corporate tax filing, accounting, bookkeeping services, payroll solutions, etc. If you are looking for an accountant Mississauga (Brampton, Toronto, GTA) or an accountancy firm Brampton, you are in the right place.

Disclaimer: The above contents are provided for general guidance only, based on information believed to be accurate and complete, but we cannot guarantee its accuracy or completeness. It does not provide legal advice, nor can it or should it be relied upon. Please contact/consult a qualified tax professional specific to your case.