![Heaader1SourceAccount[3148]](https://sourceaccounting.ca/wp-content/uploads/2021/11/Heaader1SourceAccount3148-2048x289.png)

Most entrepreneurs prefer working as an independent contractor (through a corporation) instead of working as an employee since this not only gives them the freedom of choice, but incorporation also provides many tax benefits. Hiring entities also prefer contractors over employees as they avoid paying CPP, EI, vacation, etc. Nor are they required to deduct and remit payroll source deductions to the Canada Revenue Agency (CRA).

It is a common situation in IT, construction, transportation, trucking and many other industries.

However, beware that as per the Income Tax Act, regardless of the legal form, the income is to be taxed according to the economic reality. Therefore, if you are classified as a Personal Services Business (PSB) by the CRA, your corporation will lose out on many of the tax benefits that are usually allowed for a corporation in Canada.

What happens if a corporation is classified as PSB by the CRA

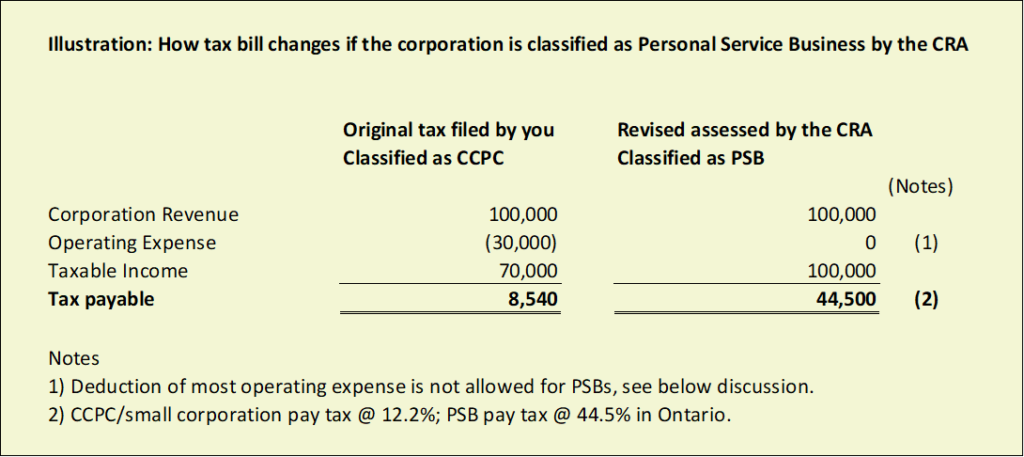

The table below is the summarized impact of being classified as PSB.

These negative consequences are discussed in detail below. But let’s first see how and why a corporation will be classified as PSB.

What makes a corporation a Personal Services Business

A PSB is a corporation that provides services to another entity that an employee of that entity would usually perform. Instead, an individual performs the services on behalf of the corporation, called an incorporated employee. And if it were not for the existence of the corporation, the person would reasonably be considered an employee of the entity receiving the services.

A Personal Services Business is a classification the CRA gives to a corporation that has the following characteristics:

- An individual performs services on behalf of the corporation.

- That individual is a shareholder (owning 10% or more) or related to a shareholder of the corporation.

- If it were not for the corporate structure, that individual would have been considered an employee of the entity hiring.

- The corporation does not employ more than 5 full-time employees throughout the year.

- The services are not being provided to an associated corporation.

However, as discussed above, income is taxed according to the economic reality, not the legal form. So, if you are the only employee of your corporation, it does not necessarily mean that you are an incorporated employee (point # 3 above). Rather, the CRA and courts have evolved four tests to determine if the relationship is of an employee or a contractor. These tests consider:

- The degree of control exercised by the employer over the duties the contractor performs.

- The degree to which the work the contractor provides is integrated with the employer’s business.

- Whether or not the employer provides the tools to be used to perform the services.

- Whether the contractor has a chance of profit, as well as the risk of loss.

The CRA and courts also take into account the intention of both parties i.e., the person performing the job and the entity hiring the contractor.

The consequence of being classified as PSB

Highest Tax Rate

PSBs don’t qualify for the small business deduction or general rate reduction that lowers the tax rate for qualified small corporations to 12.2% and for other corporations to 26.5% (in Ontario) respectively. Instead, PSBs are subject to the full corporate tax rate plus an additional 5% making the total applicable tax rate a staggering 44.5% (in Ontario).

And when the corporation passes on the income to you as dividends, you will have to pay personal taxes on the income.

Limited Deduction of expense

If the above high rate is not enough, PSB expense deductions are restricted to the following:

- salary, wages, benefits, or other remuneration of the incorporated employee

- certain expenses of the corporation associated with selling property or negotiating contracts

- legal expenses paid in the year by the corporation in collecting amounts owed for services rendered

This means PSB can’t deduct other common operating expenses that are allowable for other businesses.

CRA’s Potential Penalties

If you do not properly classify your corporation as PSB at the time of tax filing, and CRA later determines the corporation meets the criteria, the corporation could be subject to penalties and interest for filing incorrectly and paying the wrong tax rate.

How to Minimize Taxes on PSB

If you are in a situation where the employer will only hire individuals providing service through a corporation and Personal Services Business rules will apply, with its negative consequences. In that scenario, it is recommended to pay out the corporation income to you (incorporated employee) as salary. This way, income will be taxed on a personal level only at standard tax rates, avoiding the higher PSB corporate tax rate.

If your corporation wants to pay the salary/wages to you as an employee, you need to be aware of withholding and reporting obligations of an employer which mainly include the following: –

- Register a Payroll Program account with the CRA.

- Calculate income tax and CPP withholding on each payment of wages.

- Remit the employer portion of CPP contributions, income tax deducted and employee’s share of CPP contributions to the CRA timely.

- Complete and file a T4 slip and T4 Summary, due on the last day of February in the following calendar year.

- Keep records.

As you control the corporation, your salary will not be subject to EI premium, and you will not qualify for the EI benefit if you lose the contract.

How about dividends?

Dividends are paid out of corporation after-tax income, which means the PSB income would first be subject to 44.5% tax at the corporate level. On top of that, you would have to pay personal tax on the dividends issued to you. So, it is advisable, to pass the entire income as salary to avoid a very high corporate tax rate and leave nothing in the corporation to be distributed as dividends.

Final Tip – Make use of CRA’s Voluntary Disclosure Program

If you think that the corporation is PSB and you have incorrectly filed the previous returns or any there is any other discrepancy in reporting, the CRA’s Voluntary Disclosure Program (VDP) is a good option. The VDP grants relief on a case-by-case basis to taxpayers and registrants who voluntarily come forward to fix errors or omissions in their tax filings before the CRA knows or contacts them about it.

You will have to pay the taxes owing, plus interest (in part or in full) that result from your corrections. However, if CRA accepts your application, you will receive prosecution relief, and in some cases penalty relief and partial interest relief that you would have otherwise needed to pay.

If you have any questions or any other tax and accounting issues, please feel free to reach out to Source Accounting Professional Corporation (CPA). Source Accounting is a full-service accounting firm in Mississauga, dedicated to individuals, small and medium-sized businesses, providing tax preparation, corporate tax filing, accounting, bookkeeping services, payroll solutions, etc. We serve clients from Mississauga, Toronto, Brampton, Milton, Hamilton, Oakville, Etobicoke, Scarborough, and across GTA. And if you find this post helpful, please let us know in your comments.

Disclaimer: The above contents are provided for general guidance only, based on information believed to be accurate and complete, but we cannot guarantee its accuracy or completeness. It does not provide legal advice, nor can it or should it be relied upon. Please contact/consult a qualified tax professional specific to your case.